Introduction

The Phosphate Esters Market has gained increasing attention due to the compound’s exceptional performance as a flame retardant, plasticizer, and lubricant additive across numerous industrial applications. Phosphate esters are synthesized by the esterification of phosphoric acid with alcohols, resulting in versatile chemicals known for thermal stability, fire resistance, and hydrolytic stability.

From aerospace and automotive to agriculture and electronics, phosphate esters play a critical role in enhancing safety and functionality. As sustainability and industrial efficiency become central to chemical processing, the demand for high-performance and eco-friendly phosphate esters is expected to grow steadily.

Market Overview

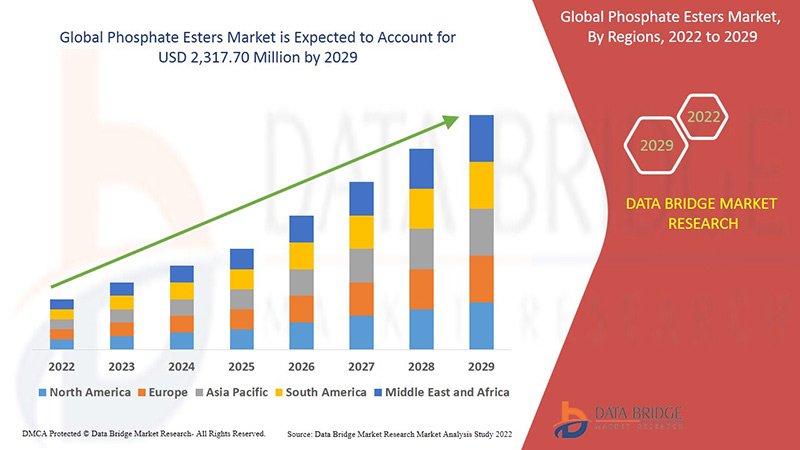

The Phosphate Esters Market was valued at USD 1.15 billion in 2024 and is projected to reach USD 1.82 billion by 2031, expanding at a CAGR of 6.8% during the forecast period. This growth is fueled by rising demand for flame-retardant materials, rapid industrialization in emerging economies, and the increasing use of phosphate-based lubricants and hydraulic fluids.

Key Market Drivers

1. Rising Demand for Flame Retardants

Phosphate esters are widely used as flame retardants in electronics, plastics, and textiles. Regulatory requirements to reduce fire hazards in public buildings, transportation systems, and consumer electronics are boosting market adoption.

2. Industrial Growth and Lubricant Usage

Their superior thermal stability makes phosphate esters ideal additives in high-performance lubricants and hydraulic fluids, particularly in heavy machinery, manufacturing plants, and aviation.

3. Shift Toward Halogen-Free Chemicals

Growing environmental concerns and regulatory bans on halogenated flame retardants have led industries to adopt halogen-free alternatives like phosphate esters, which offer similar fire-resistant properties with lower ecological risks.

4. Expansion of the Automotive and Aerospace Sectors

Both industries require reliable fire-resistant hydraulic fluids, and phosphate esters meet this demand due to their high flash points, excellent lubrication performance, and resistance to oxidation.

Market Segmentation

By Type

- Triaryl Phosphate Esters

- Alkyl Aryl Phosphate Esters

- Trialkyl Phosphate Esters

By Application

- Flame Retardants

- Hydraulic Fluids

- Lubricants

- Plasticizers

- Pesticides

- Surface Active Agents

By End Use Industry

- Automotive

- Aerospace

- Oil & Gas

- Agriculture

- Electronics

- Textiles

- Construction

- Others

Regional Insights

North America

A mature market with strong demand from the aerospace and industrial manufacturing sectors. Regulatory support for non-halogenated flame retardants also drives innovation and product adoption.

Europe

Focused on sustainable and non-toxic chemical alternatives. The EU’s REACH regulations promote phosphate ester usage over traditional flame retardants and lubricants.

Asia-Pacific

The fastest-growing region, led by China, India, and Japan. Rapid industrialization, infrastructure growth, and automotive expansion create massive demand for phosphate esters.

Middle East & Africa / Latin America

Slow but steady growth due to rising awareness about fire safety standards, and increasing chemical production capacity in select countries.

Competitive Landscape

The Phosphate Esters Market is moderately consolidated, with key players investing in R&D, capacity expansion, and product diversification. Leading companies include:

- BASF SE

- Lanxess AG

- Solvay SA

- Stepan Company

- Elementis PLC

- Eastman Chemical Company

- Dow Inc.

- AkzoNobel N.V.

- Clariant AG

- Ashland Global Holdings

Recent Developments

- Eco-Friendly Product Lines: Several manufacturers are launching bio-based phosphate esters for use in sustainable flame retardant systems and eco-lubricants.

- Advanced Hydraulic Fluids: Customized phosphate ester formulations are being developed for aircraft, heavy equipment, and military applications to meet rigorous safety standards.

- M&A Activities: Companies are consolidating market positions through mergers and acquisitions, especially to expand geographic reach in Asia-Pacific and Africa.

Challenges and Restraints

1. Environmental and Health Concerns

Some phosphate esters, particularly those with aryl groups, have been associated with toxicity and bioaccumulation risks. Regulatory scrutiny may limit their use in sensitive applications.

2. Cost Constraints

Phosphate esters are typically more expensive than conventional additives or flame retardants, which may deter adoption in cost-sensitive markets.

3. Supply Chain Volatility

Fluctuations in raw material prices and geopolitical risks (especially in phosphate rock mining regions) can impact production and pricing stability.

Future Trends

1. Bio-Based and Green Alternatives

The development of renewable phosphate ester solutions derived from vegetable oils or biodegradable alcohols is expected to gain momentum, aligning with sustainability goals.

2. Smart Flame Retardant Systems

Emerging technologies involve integrating phosphate esters into smart polymers that react to temperature or flame exposure, offering enhanced safety and performance.

3. Digital Monitoring of Fluid Performance

Integration of sensors and AI in industrial equipment enables real-time monitoring of phosphate ester-based fluids, improving maintenance schedules and reducing system failures.

Conclusion

The Phosphate Esters Market is poised for steady growth driven by heightened safety standards, eco-regulatory trends, and performance benefits across diverse industries. As flame retardancy, lubrication efficiency, and sustainability become non-negotiable requirements, phosphate esters are likely to become indispensable in advanced manufacturing and chemical formulation.

Market stakeholders focusing on innovation, regulatory compliance, and strategic regional expansion will be well-positioned to capitalize on emerging opportunities in this dynamic sector.

Get More Details : https://www.databridgemarketresearch.com/reports/global-phosphate-esters-market

Get More Reports :

Related Reads

- Custom Fitness App Development: Build the Fitness App Your Users Actually Want

- Hoodie Outfits Gaining Popularity This Season

- Yes or No Tarot – Discover Quick Answers with Yes or No Decision Wheel

- SASE Platforms Market 2030: Size, Growth Drivers & Competitive Landscape

- Trapstar Windbreakers: Style Meets Function in Every Season

- What Tempo Signifies in Driver Shafts for Sale